Ridge and Lasso in R

A common and very challenging problem in machine learning is overfitting, and it comes in many different appearances. It is one of the major aspects of training the model. Overfitting occurs when the model is capturing too much noise in the training data set which leads to bad predication accuracy when applying the model to new data. One of the ways to avoid overfitting is regularization technique.

In this tutorial, we will examine Ridge regression and Lasso which extend the classical linear regression. Earlier, we have shown how to work with Ridge and Lasso in Python, and this time we will build and train our model using R and the caret package.

Like classical linear regression, Ridge and Lasso also build the linear model, but their fundamental peculiarity is regularization. The goal of these methods is to improve the loss function so that it depends not only on the sum of the squared differences but also on the regression coefficients.

One of the main problems in the construction of such models is the correct selection of the regularization parameter. Comparing to linear regression, Ridge and Lasso models are more resistant to outliers and the spread of data. Overall, their main purpose is to prevent overfitting.

The main difference between Ridge regression and Lasso is how they assign a penalty to the coefficients. We will explore this with our example, so let’s start.

We will work with the Diamonds dataset, which you can download from the next website: http://vincentarelbundock.github.io/Rdatasets/datasets.html. It contains the prices and other attributes of almost 54,000 diamonds. We will be predicting the price of diamonds using other attributes and compare the results for Ridge, Lasso, and OLS.

# Upload the dataset

diamonds <-read.csv('diamonds.csv', header = TRUE, sep = ',')

head(diamonds)## X carat cut color clarity depth table price x y z

## 1 1 0.23 Ideal E SI2 61.5 55 326 3.95 3.98 2.43

## 2 2 0.21 Premium E SI1 59.8 61 326 3.89 3.84 2.31

## 3 3 0.23 Good E VS1 56.9 65 327 4.05 4.07 2.31

## 4 4 0.29 Premium I VS2 62.4 58 334 4.20 4.23 2.63

## 5 5 0.31 Good J SI2 63.3 58 335 4.34 4.35 2.75

## 6 6 0.24 Very Good J VVS2 62.8 57 336 3.94 3.96 2.48# Drop the index column

diamonds<- diamonds[ , -which(names(diamonds)=='X')]

head(diamonds)## carat cut color clarity depth table price x y z

## 1 0.23 Ideal E SI2 61.5 55 326 3.95 3.98 2.43

## 2 0.21 Premium E SI1 59.8 61 326 3.89 3.84 2.31

## 3 0.23 Good E VS1 56.9 65 327 4.05 4.07 2.31

## 4 0.29 Premium I VS2 62.4 58 334 4.20 4.23 2.63

## 5 0.31 Good J SI2 63.3 58 335 4.34 4.35 2.75

## 6 0.24 Very Good J VVS2 62.8 57 336 3.94 3.96 2.48# Print unique values of text features

print(levels(diamonds$cut))## [1] "Fair" "Good" "Ideal" "Premium" "Very Good"print(levels(diamonds$clarity))## [1] "I1" "IF" "SI1" "SI2" "VS1" "VS2" "VVS1" "VVS2"print(levels(diamonds$color))## [1] "D" "E" "F" "G" "H" "I" "J"As you can see, there is a finite number of variables, so we can change these categorical variables to numerical.

diamonds$cut <- as.integer(diamonds$cut)

diamonds$color <-as.integer(diamonds$color)

diamonds$clarity <- as.integer(diamonds$clarity)

head(diamonds)## carat cut color clarity depth table price x y z

## 1 0.23 3 2 4 61.5 55 326 3.95 3.98 2.43

## 2 0.21 4 2 3 59.8 61 326 3.89 3.84 2.31

## 3 0.23 2 2 5 56.9 65 327 4.05 4.07 2.31

## 4 0.29 4 6 6 62.4 58 334 4.20 4.23 2.63

## 5 0.31 2 7 4 63.3 58 335 4.34 4.35 2.75

## 6 0.24 5 7 8 62.8 57 336 3.94 3.96 2.48Before building the models, let’s first scale data.

Scaling will put the ranges of our features from -1 till 1. Thus a feature with a larger scale won’t have a larger impact on the target variable.

To scale a feature we need to subtract the mean from every value and divide it by standard deviation.

For scaling data and training the models we’ll use caret package. The caret package (short for Classification And REgression Training) is a wrapper around a number of other packages and provides a unified interface for data preparation, models training, and metrics evaluation.

# Create features and target matrixes

X <- diamonds %>%

select(carat, depth, table, x, y, z, clarity, cut, color)

y <- diamonds$price

# Scale data

preprocessParams<-preProcess(X, method = c("center", "scale"))

X <- predict(preprocessParams, X)Now, we can basically build Lasso and Ridge. We’ll split the data into a train and a test dataset but for now we won’t set the regularization parameter lambda. It is set to 1.

The “glmnet” method in caret has an alpha argument that determines what type of model is fit. If alpha = 0 then a ridge regression model is fit, and if alpha = 1 then a lasso model is fit. Here we’ll use caret as a wrapper for glment.

# Spliting training set into two parts based on outcome: 75% and 25%

index <- createDataPartition(y, p=0.75, list=FALSE)

X_train <- X[ index, ]

X_test <- X[-index, ]

y_train <- y[index]

y_test<-y[-index]# Create and fit Lasso and Ridge objects

lasso<-train(y= y_train,

x = X_train,

method = 'glmnet',

tuneGrid = expand.grid(alpha = 1, lambda = 1)

)

ridge<-train(y = y_train,

x = X_train,

method = 'glmnet',

tuneGrid = expand.grid(alpha = 0, lambda = 1)

)

# Make the predictions

predictions_lasso <- lasso %>% predict(X_test)

predictions_ridge <- ridge %>% predict(X_test)

# Print R squared scores

data.frame(

Ridge_R2 = R2(predictions_ridge, y_test),

Lasso_R2 = R2(predictions_lasso, y_test)

)## Ridge_R2 Lasso_R2

## 1 0.8584854 0.8813328# Print RMSE

data.frame(

Ridge_RMSE = RMSE(predictions_ridge, y_test) ,

Lasso_RMSE = RMSE(predictions_lasso, y_test)

)## Ridge_RMSE Lasso_RMSE

## 1 1505.114 1371.852# Print coeficients

data.frame(

as.data.frame.matrix(coef(lasso$finalModel, lasso$bestTune$lambda)),

as.data.frame.matrix(coef(ridge$finalModel, ridge$bestTune$lambda))

) %>%

rename(Lasso_coef = X1, Ridge_coef = X1.1)## Lasso_coef Ridge_coef

## (Intercept) 3934.27842 3934.23903

## carat 5109.77597 2194.54696

## depth -210.68494 -92.16124

## table -207.38199 -156.89671

## x -1178.40159 709.68312

## y 0.00000 430.43936

## z 0.00000 423.90948

## clarity 499.77400 465.56366

## cut 74.61968 83.61722

## color -448.67545 -317.53366These two models give very similar results. Now let’s choose the regularization parameter with the help of tuneGrid. The models with the highest R-squared score will give us the best parameters.

parameters <- c(seq(0.1, 2, by =0.1) , seq(2, 5, 0.5) , seq(5, 25, 1))

lasso<-train(y = y_train,

x = X_train,

method = 'glmnet',

tuneGrid = expand.grid(alpha = 1, lambda = parameters) ,

metric = "Rsquared"

)

ridge<-train(y = y_train,

x = X_train,

method = 'glmnet',

tuneGrid = expand.grid(alpha = 0, lambda = parameters),

metric = "Rsquared"

)

linear<-train(y = y_train,

x = X_train,

method = 'lm',

metric = "Rsquared"

)

print(paste0('Lasso best parameters: ' , lasso$finalModel$lambdaOpt))## [1] "Lasso best parameters: 2.5"print(paste0('Ridge best parameters: ' , ridge$finalModel$lambdaOpt))## [1] "Ridge best parameters: 25"predictions_lasso <- lasso %>% predict(X_test)

predictions_ridge <- ridge %>% predict(X_test)

predictions_lin <- linear %>% predict(X_test)

data.frame(

Ridge_R2 = R2(predictions_ridge, y_test),

Lasso_R2 = R2(predictions_lasso, y_test),

Linear_R2 = R2(predictions_lin, y_test)

)## Ridge_R2 Lasso_R2 Linear_R2

## 1 0.8584854 0.8813317 0.8813157data.frame(

Ridge_RMSE = RMSE(predictions_ridge, y_test) ,

Lasso_RMSE = RMSE(predictions_lasso, y_test) ,

Linear_RMSE = RMSE(predictions_ridge, y_test)

)## Ridge_RMSE Lasso_RMSE Linear_RMSE

## 1 1505.114 1371.852 1505.114print('Best estimator coefficients')## [1] "Best estimator coefficients"data.frame(

ridge = as.data.frame.matrix(coef(ridge$finalModel, ridge$finalModel$lambdaOpt)),

lasso = as.data.frame.matrix(coef(lasso$finalModel, lasso$finalModel$lambdaOpt)),

linear = (linear$finalModel$coefficients)

) %>% rename(lasso = X1, ridge = X1.1)## lasso ridge linear

## (Intercept) 3934.23903 3934.27808 3934.27526

## carat 2194.54696 5103.53988 5238.57024

## depth -92.16124 -210.18689 -222.97958

## table -156.89671 -207.17217 -210.64667

## x 709.68312 -1172.30125 -1348.94469

## y 430.43936 0.00000 23.65170

## z 423.90948 0.00000 22.01107

## clarity 465.56366 499.73923 500.13593

## cut 83.61722 74.53004 75.81861

## color -317.53366 -448.40340 -453.92366Our score raised a little, but with these values of lambda, there is not much difference. Let’s build coefficient plots to see how the value of lambda influences the coefficients of both models.

We will use glmnet function to train the models and then we’ll use plot() function that produces a coefficient profile plot of the coefficient paths for a fitted “glmnet” object.

Xvar variable of plot() defines what is on the X-axis, and there are 3 possible values it can take: “norm”, “lambda”, or “dev”, where “norm” is for L1-norm of the coefficients, “lambda” for the log-lambda sequence, and “dev” is the percent deviance explained. We’ll set it to lambda.

To train glment, we need to convert our X_train object to a matrix.

# Set lambda coefficients

paramLasso <- seq(0, 1000, 10)

paramRidge <- seq(0, 1000, 10)

# Convert X_train to matrix for using it with glmnet function

X_train_m <- as.matrix(X_train)

# Build Ridge and Lasso for 200 values of lambda

rridge <- glmnet(

x = X_train_m,

y = y_train,

alpha = 0, #Ridge

lambda = paramRidge

)

llaso <- glmnet(

x = X_train_m,

y = y_train,

alpha = 1, #Lasso

lambda = paramLasso

)## Warning: Transformation introduced infinite values in continuous x-axis

## Warning: Transformation introduced infinite values in continuous x-axis

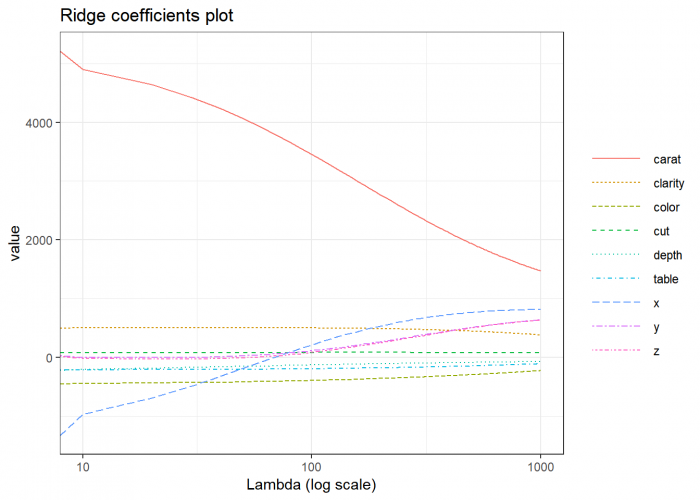

As a result, you can see that when we raise the lambda in the Ridge regression, the magnitude of the coefficients decreases, but never attains zero. The same scenario in Lasso influences less on the large coefficients, but the small coefficients are reduced to zeroes.

We can conclude from the plot that the “carat”" feature has the most impact on the target variable. Other important features are “clarity” and “color” while features like “z” and “cut” have barely any impact.

Therefore Lasso can also be used to determine which features are important to us and have strong predictive power. The Ridge regression gives uniform penalties to all the features and in such way reduces the model complexity and prevents multicollinearity.

Now, it’s your turn!